401(k)

Benefits Enrollment & Changes

You may enroll or make changes to your 401(k) contributions anytime during the year. No change in status is required, and there is no special annual enrollment period for this plan. However, the annual open enrollment period (November 1 - 15) is a good time to take a moment to review your current contribution levels and investments, and make changes if needed.

401(k) elections & changes (including beneficiary designations) are made on the T Rowe Price website (not in Workday).

To view the slides from the T, Rowe Price Roth Contributions presentation held on 1/8/26 and 1/14/26, click HERE or in the link under the PDFs section of this page. The FAQs from both presentations will be posted to this page under PDFs soon.

Maritz Investment Plan 401(k)/ T. Rowe Price

The Maritz Investment Plan (MIP) is available for regular full-time and regular part-time employees. Part-time employees are eligible to participate once they have worked 500 hours in a calendar year. This 401(k) benefit plan allows employees to accumulate funds for future financial security through special investment opportunities while sheltering part of your salary from taxes today.

By participating in the plan, you authorize Maritz, through payroll deductions, to contribute a portion of your pay (determined by you) to your MIP account on a before-tax basis. You can also make after-tax contributions to the plan. All contributions can be invested in one or a combination of T. Rowe Price investment funds of your choice.

Go to the T. Rowe Price portal to enroll, change current elections, rollover funds from a prior 401(k), request a loan or hardship withdrawal, change investment options, add or change your 401(k) beneficiary, or review your balance.

401(k) Contributions & Changes

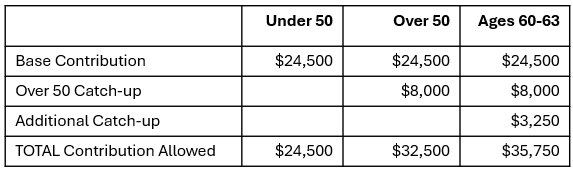

You are eligible to contribute up to 90% of your compensation pre-tax and/or Roth after-tax, up to an annual contribution limit of $24,500 (for those under age 50) for 2026. The catch-up limit for those aged 50 and older allows for an extra $8,000, for a combined total contribution limit of $32,500. If you fall in the age range of 60 - 63, you are allowed an additional catch-up amount (above the age 50 and older amount) of $3,250, for a combined total contribution limit of $35,750.

You are also eligible to contribute up to 6% of your compensation on an after-tax (non-Roth) basis. However, the total pre-tax, Roth, and non-Roth after-tax contributions cannot exceed 90% of your compensation.

You have the option to roll prior employee pre-tax contributions or non-Roth after-tax contributions over to Roth. However, keep in mind that the amount of your pre-tax in-plan Roth rollover will be taxable to you in the calendar year of the rollover and could push you into a higher tax bracket. Taxes will not be withheld at the time of the rollover. You will receive a 1099-R in January from T. Rowe Price listing total Roth contributions and will need to pay any applicable taxes when you file your annual tax return. We strongly recommend that you consult with a tax advisor/counsel before electing an in-plan rollover of your pre-tax contributions to Roth. To elect an in-plan Roth rollover, log in to your T. Rowe Price portal, then select Take Action at the top, then select Start In-Plan Roth Rollover.

Company Matching Contributions

With matching contributions, for every pre-tax or Roth dollar you contribute up to 2% of your eligible base and bonus pay, Maritz will contribute one dollar to your Plan account each pay period. For the next 5% of your eligible pay you contribute, the company will match 50 cents for every dollar. If you defer 7% for your employee contribution, Maritz will add 4.5%. There is no company match on your non-Roth after-tax contributions.

Company match dollars will be sent to T. Rowe Price as pre-tax. You have the option to have T. Rowe Price convert your company match from pre-tax to Roth after-tax. If you are interested in this option, log in to your T. Rowe Price portal and select Take Action at the top. Then select Manage Roth Employer Contributions and click on the button next to the Roth Employer Match, Company Matching Contributions to slide that bar from “off” to “on”.

Please note that you must be 100% vested to convert company match dollars from pre-tax to Roth. If you are not vested, then you will not have the option to change that setting in the portal.

Once employer matching contributions have been converted from pre-tax to Roth, they cannot later be converted back to pre-tax.

Electing to receive employer contributions as Roth will increase your taxable income, so you may want to consult a tax advisor before completing this transaction. Taxes on these contributions are not withheld each pay period and have to be paid annually with your income tax. You will receive a Form 1099-R from T. Rowe Price in January reflecting the total amount of Roth employer contributions contributed each year. You have the option to have additional voluntary withholding from each paycheck to cover your taxes and to help avoid an under withholding penalty. To add additional voluntary withholding, log in to Workday and select the Benefits and Pay app, then in the left column under Suggested Links, select Maintain Withholding Elections (BSI).

|

Your Pre-Tax Contribution and/or Roth Percentage |

Maritz Matching Percentage |

|

1% |

1% |

|

2% |

2% |

|

3% |

2.5% |

|

4% |

3% |

|

5% |

3.5% |

|

6% |

4% |

|

7% |

4.5% |